The Paul Ryan PowerPoint presentation about healthcare is excellent

Republicans attempting to repeal Obamacare and replace it with the American Health Care Act are taking a pummeling. Everyone from the American Medical Association and the AARP to the Tea Party Patriots have come down against it. House Speaker Paul Ryan took to PowerPoint to explain and defend the law, and his presentation technique was quite effective.

Let me be clear here — I don’t think Ryan’s AHA is the right solution. And Ryan did not, in his presentation, address problems like subsidies based on age rather than income, or whether Health Savings Accounts and tax credits would be an effective substitute the mandate that individuals must have health insurance.

But I’m not here to debate the proposed bill (on which most of you have already made up your minds). My question is: did Paul Ryan make his case for it well? And in contrast to soundbite-driven, fact-impaired screaming I see — and the oversimplified horserace-focused coverage in major media outlets — Ryan’s presentation was clear, well-thought-out, well-structured, and fact-based. Yes, I know that Twitter is going nuts with photoshopped versions that replace the slides with jokes that ridicule Republicans. But if you actually care about the facts, you should review the video of the presentation on CNN (it’s also embedded at the bottom of this post).

Ryan’s PowerPoint was well structured

A good presentation is easy to follow; it tells you what’s coming and then delivers it. Ryan followed this formula. He explained how the AHA fits in with other legislative priorities, and followed that up with a description of what’s going wrong with the Affordable Care Act and how the AHA would fix that problem. And from watching this, I learned a few things.

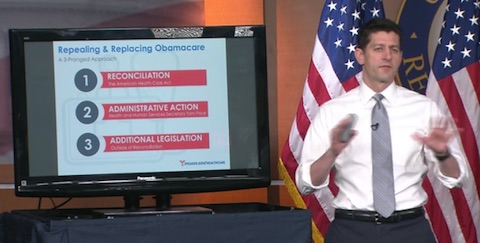

Ryan’s presentation started with this slide:

Ryan used this to make the point that the AHA is not the whole strategy. AHA includes only the elements that can use the Reconciliation process in the Senate to avoid Democrats blocking them with a filibuster. In the second step, President Trump and Health and Human Services Secretary Tom Price use executive power to change some rules, and in the third step Congress passes additional laws that can’t go through the reconciliation process. In stage 3 is when Ryan foresees enabling national associations of, for example, restaurateurs to create healthcare plans available to all of their members across state lines. All of the media discussion I’ve seen focuses only on the first stage and AHA.

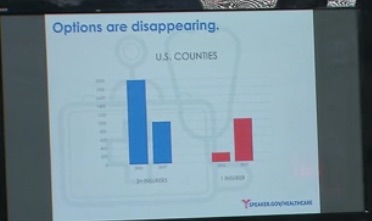

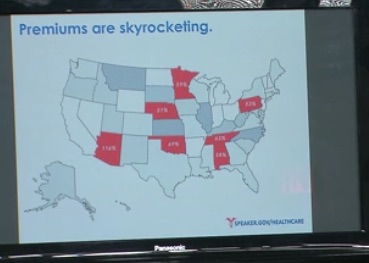

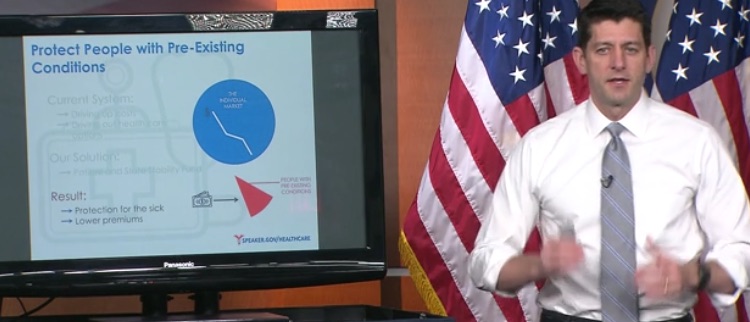

Ryan and the Republicans need to convince you that the Affordable Care Act (which, of course, he refers to only as “Obamacare”) is failing. Ryan’s charts showing the decrease in counties with 3 choices in their exchanges, the increase in counties with only one choice, and cost increases in some states, are effective. I’ll get to the readability problems in a moment, but Ryan did actually describe the numbers on these slides, signs of a significant problem.

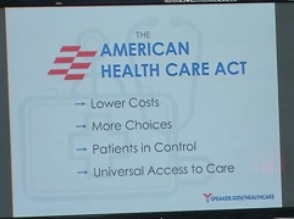

Another principle of effective PowerPoint is to provide signposts with slides that lay out sections. Ryan (or whichever of his aides put this together) does that well. Here’s the slide at the start of the section describing what’s in the American Health Care Act.

In this section I learned something I didn’t know: that Republicans are advocating a different approach to spreading risk. In the current approach, the individual mandate attempts to get as may healthy people into the insurance pool as possible, so that they can help subsidize the costly care for those with expensive conditions. This approach only works if you can, indeed, get the healthy people in — if you can’t, the costs go way up, which creates the insurance premium “death spiral.” Ryan proposes separating those with preexisting conditions into a high risk pool, which would keep costs low for those not in the pool. Of course he doesn’t talk about the costs for the high-risk pool. But I’d like to hear more about this approach, and I haven’t heard any public discussion of it at all.

Ryan mixes slides with narration well

For Paul Ryan, this is a unique opportunity to speak directly to the electorate. He did that well.

If you present technical material with PowerPoint or a similar product, take a look at how his voiceover complements the slides. Ryan does not read the slides, but he refers to them. He uses animation to make points, not to create eye-candy. And he looks at and speaks directly to the audience, using changes in the tone of voice and pace to indicate when he’s explaining, when he’s trying to be convincing, and when he is trying to be sincere. At the end, he clearly takes responsibility for Republicans taking this moment to save American healthcare.

I’d be more inclined to vote for a politician who took the time to explain things this way, over those that just throw red-meat slogans at their bases. I like problem-solvers.

Ryan’s PowerPoint has a few flaws

If I were coaching Ryan, here are few changes I’d suggest:

- Bigger type. Given the way he presented — talking next to a TV screen in a well-lit room — Ryan’s slides are flawed. Even though the amount of text is limited, it’s too small and you can’t read it.

- Go wide. It’s been an HD world for a while now. All PowerPoint slides should be 16:9 aspect ratio. He’s wasting the space at the sides of the screen, and that’s idiotic. If you’re still doing your PowerPoints in 4:3 ratio, please join the rest of us in the 21st Century.

- Put it on SlideShare. I’d really like to see the actual slides and not just CNN’s video of them, but the PowerPoint is not available online.

- Address objections. There’s a lot wrong with the AHA, which is why so many groups have come down against it. If there are objections, as a speaker, you have a responsibility to anticipate and address them. Ryan’s presentation would be far more effective if he did that.

Go to the source

If you as a citizen really want to understand the debate at more than a sound-bite level, you ought to review content like this when it’s available. The New York Times and Wall Street Journal didn’t address Ryan’s points from this presentation at all, choosing to focus instead on which Republicans might or might not support it. I’d like to know what people are voting on, with perspective from both sides, not just how they’re voting.

One final note before you see the video. I will delete partisan comments about how great or awful the Republican and their healthcare plan are — unsurprisingly, we’re not going to settle that issue in the comments section of my site. The topic of this post is: did Ryan make his points well or poorly, did the media cover that, and did you learn anything?

Josh, thanks to you I watched the entire presentation, and yes, it was very well executed from a communications point of view. Ryan sets up what consultants call a “burning platform” — this issue is on fire, etc. — and then explains clearly how the GOP plans to put the fire out.

I do think there was one whiff of bullshit, which I’ll try to state apolitically so you don’t delete me. I refer to this type of BS as *Invisible Bullshit.* Invisible BS isn’t what you say that’s wrong. It’s what you don’t say that you don’t want to admit is wrong.

Here, the Invisible BS is payment for the high-risk population, the pie chart “red slice.” Ryan does a great job explaining Obamacare is failing because the risk pool is not big enough (not enough healthy people signed up) to pay for the sick people who need healthcare. Ryan then notes that 1% of the covered account for 23% of healthcare costs.

His solution is to remove that 1% red slice from the insurance pool, and have them be paid for by some form of reinsurance and government payments. Then healthcare costs will stabilize for the rest, and the free market will work.

And this is where the invisibility rhetorical trick comes in.

How much will that cost, to cover that “red slice” of sick people? And who will pay for it? The government directly, via taxes? Ryan alludes to this at 15:27 then moves quickly past. This is not a minor point. This is the core group of sick people who, Ryan states, without others paying in, have driven up costs. If Ryan is removing them from the insurance pool, where do those sick people go? Will they be covered by a big government program? Medicare pushed downward? Will taxes pay for this? I’m intrigued by the idea, but I really want to know.

My point is not to debate policy, but to note that Ryan takes time to pinpoint a core issue — one group of sick people is driving up costs without others paying in to cover them — and then moves them all, in a red piechart slice, off to the side, and say, solved!

When you define a problem and then your solution is to make the core of the problem turn invisible, that’s a type of Invisible BS.

Great points, Ben. I like what you say about “invisible BS” and there’s definitely some of that in this presentation.

He’s doing exactly what the insurance companies do… move people whose house is already burning out of the fire insurance pool. You’re right that it does beg the question of who pays for the firefighting in those cases, but the government (when they’re not pointing fingers at the “greedy” insurers) can see the problem just as clearly as the private sector actuaries.

I agree it was a good presentation despite opening himself up for all manner of jokes. I watched this in real time and the way he delivered the information was helpful in that it was easy to see where the holes were. This may be why politicians avoid this kind of honesty. I also agree with the “invisible BS” handwaving elements Ben mentioned above.

Support a lot of bullshit with a good deck. Call that the Fiber Imperative.

After watching the entire Ryan presentation, several things are clear. First, including former House Speaker Pelosi and Majority Leader Reid, Ryan is the first Speaker/Party leader with sufficient economic literacy to intelligently critique the ACA and its pending collapse. Second, Ryan deserves credit for clearly disclosing the penalty all policy buyers confront when relying exclusively on OPM – other people’s money. Third, the budgetary “black hole” associated with high risk pools will, by its very nature, be iterative and akin to property and casualty coverage in hurricane and flood zones. The tax payer has been and will always be the insurer of last resort.